The Fundamentals of Performance Management

June 15, 2021New Mandatory Preventive Items and Services

June 28, 2021

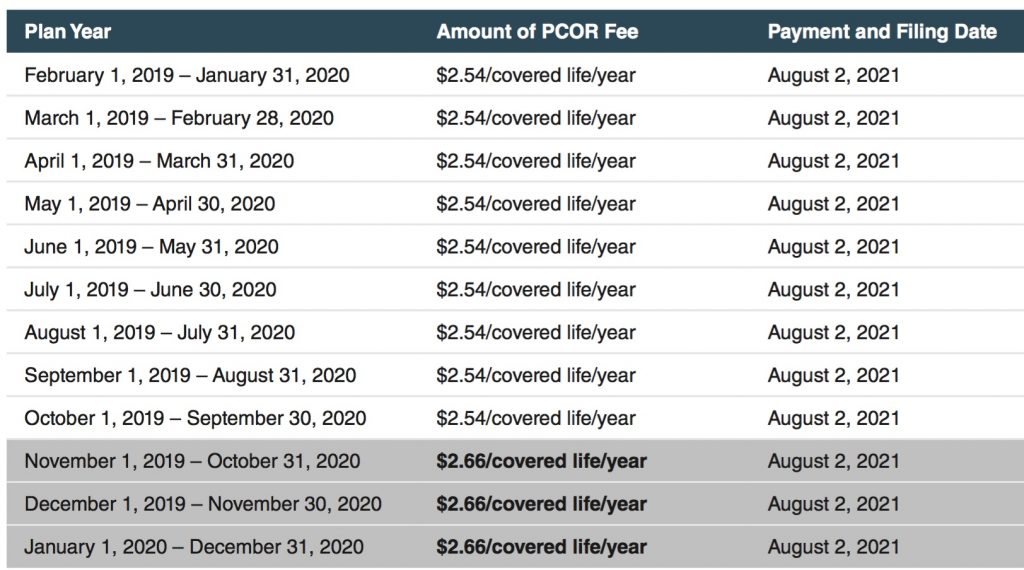

The Patient-Centered Outcomes Research (PCOR) fee filing deadline is August 2, 2021, for all self-funded medical plans and HRAs for plan years ending in 2020. The IRS issued Notice 2020-84 announcing the adjusted fee amount for this year as well as limited transition relief.

The plan years and associated amounts are as follows:

Employers with self-funded health plans ending in 2020 should use the 2nd quarter Form 720 to file and pay the PCOR fee by August 2, 2021. The information is reported in Part II.

Please note that Form 720 is a tax form (not an informational return form such as Form 5500). As such, the employer or an accountant would need to prepare it. Parties other than the plan sponsor, such as third-party administrators and USI, cannot report or pay the fee.

Temporary Transition Relief

Generally, there are three established methods a self-funded group health plan may use to determine the average number of covered lives for purposes of calculating the PCOR fee:

- The Actual Count Method,

- The Snapshot Method, and

- The Form 5500 method. For plan years that end on or after October 1, 2019 and before October 1, 2020, in addition to the established counting methods, a plan may use any reasonable method for calculating the average number of covered lives. This relief has not been extended.

Mark J. Goldstein / 610-674-0990 / Goldmark Benefits / service@goldmarkbenefits.com

This blog is designed to highlight various employee benefit matters of general interest to our readers. It is not intended to interpret laws or regulations, or to address specific client situations. You should not act or rely on any information contained herein without seeking the advice of an attorney or tax professional. ©2021 Emerson Reid, LLC. All Rights Reserved. CA Insurance License #0C94240.

{kind=link}

{kind=link}

{kind=link}